By Chloe Mari A. Hufana and Aubrey Rose A. Inosante, Reporters

PHILIPPINE PRESIDENT Ferdinand R. Marcos, Jr. on Monday appointed Finance Secretary Ralph G. Recto as the new executive secretary and economic czar Frederick D. Go to take over the Finance department, marking the biggest Cabinet shake-up since the eruption of the multibillion-peso flood control scandal.

“These leadership changes reinforce the President’s commitment to strengthening institutions, improving coordination across government, and keeping the administration focused on delivering stability, opportunity, and security to Filipino families,” Palace Press Officer Clarissa A. Castro told a news briefing.

The appointments were announced after Mr. Marcos accepted the resignation of Executive Secretary Lucas P. Bersamin and Budget Secretary Amenah F. Pangandaman.

“Both officials respectfully offered and tendered their resignations out of delicadeza, after their departments were mentioned in allegations related to the flood control anomaly currently under investigation and in recognition of the responsibility to allow the administration to address the matter appropriately,” Ms. Castro said.

She said Mr. Recto’s extensive background in economic legislation and national planning “positions him well” to oversee day-to-day government operations and coordinate high-impact programs as executive secretary.

Sought for comment at the Senate, Mr. Recto told reporters he had not talked to the President.

“I’m surprised but work has to continue. Essentially, I think the role of the [executive secretary] is governance… You cannot do miracles. Our job is to improve governance,” Mr. Recto said.

Concerning Mr. Go’s appointment as Finance chief, Ms. Castro cited his role in “advancing investments, strengthening investor confidence, and aligning economic initiatives across agencies.”

In a statement, Mr. Go thanked the President for his “continuing trust and confidence.”

“Recognizing the challenges and opportunities ahead, I am fully committed to promoting fiscal strength and sustainable economic growth for the country,” Mr. Go said.

There is no replacement yet for Mr. Go, who held the title of special assistant to the President for investment and economic affairs.

Budget Undersecretary Rolando U. Toledo will be the officer in charge at the Department of Budget and Management (DBM).

“(Mr. Toledo’s) designation ensures uninterrupted operations as the government prepares for the rollout of next year’s budget, ongoing recovery efforts in disaster-affected regions, and the continued funding of social and economic programs,” Ms. Castro said.

The Philippine government is investigating a multibillion-peso public works scandal that Mr. Marcos exposed during his State of the Nation Address in July. Government officials and lawmakers have allegedly colluded with private contractors to receive billions of kickbacks from public works projects.

Rizal Commercial Banking Corp. Chief Economist Michael L. Ricafort said Mr. Recto is signaling a focus on governance reforms.

“Drawing on his 20 years of experience in fiscal and policy measures, Mr. Recto’s serious pursuit of anti-corruption initiatives and higher governance standards — similar to efforts 10-15 years ago — could have positive effects on the local economy and financial markets,” he said.

GROWTH AT 4.7%Prior to the announcement of his appointment as executive secretary, Mr. Recto said the Philippine economy is likely to expand by at least 4.7% this year.

In a statement sent Monday morning, he said the economy remains “fundamentally strong,” backed by stable foundations, investment opportunities, and growth faster than the “true cost” of debt.

“By the end of 2025, the real interest rate we pay is estimated at only 3.3%, while our economy is expected to grow by 4.7% to 4.8%,” Mr. Recto said.

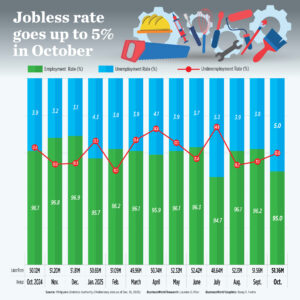

Philippine gross domestic product (GDP) growth averaged 5% in the first nine months, falling short of the government’s 5.5-6.5% target for 2025.

The government’s sweeping corruption crackdown since August has hurt economic growth as well as consumer and investor confidence.

“We are not blind to the challenges, nor are we shaken by them. What you see today is not a leadership crisis, but a government reforming itself from within, led by a President who chose to be the whistleblower, not the apologist, of corruption,” Mr. Recto said.

He stressed that trust is the lifeblood of any economy.

“It keeps investments flowing, businesses expanding, and jobs growing. That trust is being protected, strengthened, and rebuilt every single day under the Marcos administration,” he said.

Mr. Recto, who is part of the Monetary Board, said weak inflation gives the Bangko Sentral ng Pilipinas (BSP) more room to cut interest rates, supporting household spending and economic growth.

“Above all, we assure the Filipino people that our fiscal consolidation path is on track, and everything moving forward is on the upside,” he said, noting that the government will bring down the deficit and debt gradually.

The Marcos administration is targeting to reduce the fiscal deficit to 5.5% of GDP in 2025, with the gap projected to ease further to 3.1% by 2030.

The country’s outstanding debt stood at P17.46 trillion at end-September but still remained above the P17.36-trillion full-year program.