THE NATIONAL GOVERNMENT (NG) remains on track with its medium-term fiscal consolidation program even as it continues to borrow to help spur economic growth and as its debt remains at a record high due to loans racked up during the coronavirus pandemic.

Finance Secretary Ralph G. Recto said at a Congress hearing in August that the Philippine economy, as measured by its gross domestic product (GDP), is on track to outgrow its debt as targeted under its medium-term fiscal consolidation framework.

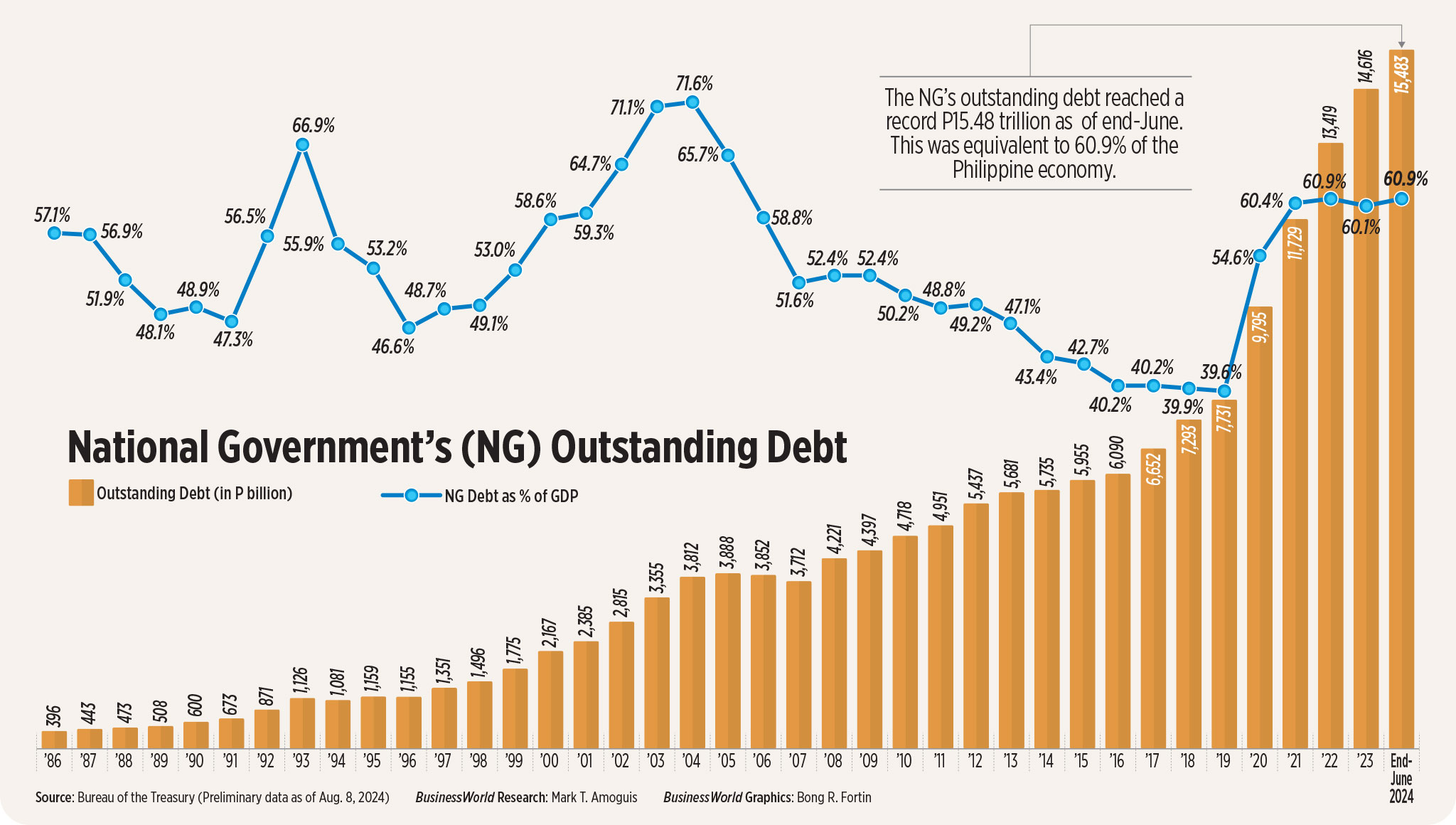

“From 60.9% (debt-to-GDP ratio) in 2022, it fell to 60.1% in 2023. And we are determined to continue pushing it below 60% so we have enough buffer in case another crisis hits us,” Mr. Recto said. “The continuous decline in our debt-to-GDP ratio since the pandemic is one of the reasons why our credit ratings remain high… This means that we not only have the capacity to pay our debts, but we can have more access to cheaper financing.”

The debt-to-GDP threshold considered by multilateral lenders to be manageable for developing economies is 60%.

The Finance chief said the government is still paying off borrowings made during the coronavirus pandemic, resulting in narrower fiscal space.

“There is nothing inherently wrong with a country having debt, as long as the money’s used for the right purposes, such as growing the economy, which in turn creates more jobs, increases income and provides more revenues for the government,” he said. “In our case, we are using debts to spur our stronger economic recovery by investing in more infrastructure and human capital development projects which have the highest multiplier effect on the economy.”

According to data from the Bureau of the Treasury, the government’s outstanding debt stood at just P7.73 trillion at end-2019 or before the coronavirus pandemic, accounting for 39.6% of GDP. The economy expanded by 6.1% annually that year.

This jumped to P9.795 trillion by end-2020 or 54.6% of GDP as the government borrowed to help support the economy — which contracted by 9.5% that year — and fund its spending needs during the health crisis.

Indebtedness further ballooned to P11.73 trillion as of 2021 (60.4% of GDP) and to P13.42 trillion by end-2022 (60.9%). This came even as the economy rebounded, growing by 5.7% in 2021 and by 7.6% in 2022.

At end-2023, the NG debt level rose 0.7% annually to P14.62 trillion, although its share in GDP inched down to 60.1%. GDP growth slowed to 5.5% last year.

As of end-June 2024, the NG’s outstanding debt stood at a fresh record high of P15.48 trillion, up 9.4% from a year ago. This translated to a debt-to-GDP ratio of 60.9% as the economy expanded by 6% annually in the first half.

The government set a debt-to-GDP ratio target of 60.6% for this year as its outstanding debt level is expected to reach P16.06 trillion and as it aims for 6-7% economic growth.

Under the Development Budget Coordination Committee’s (DBCC) updated medium-term fiscal program, the government aims to bring this ratio down to 60.4% by end-2025, 60.2% in 2026, 58.4% in 2027 and 56.3% in 2028. This, as it targets GDP growth of 6.5-7.5% in 2025 and 6.5-8% from 2026 to 2028.

“We make sure that when we do our borrowing, we take into account all these debt management objectives of making sure that we manage our refinancing risk, and our interest rate risk exposure is minimal,” National Treasurer Sharon P. Almanza told BusinessWorld via telephone.

Under its revised fiscal framework, the government wants to maintain an 80:20 borrowing mix in favor of domestic sources until 2028 to lessen foreign exchange risks, Ms. Almanza said.

Around 80% of the government’s current obligations have long-term maturities, making its current debt structure manageable, she added.

“So long as the economy is growing more than the cost of our borrowing, we are still able to reduce our debt ratio.”

Debt watcher Fitch Ratings said strong nominal GDP growth and narrowing budget deficits should help bring down the share of debt in the Philippine economy over the medium term.

The government has capped its budget deficit at P1.48 trillion this year, which is equivalent to 5.6% of GDP. The ratio is expected to gradually go down over the next four years to 5.3% in 2025, 4.7% in 2026, 4.1% in 2027, and then to 3.7% of GDP by 2028, closer to the pre-pandemic levels of 2-3%.

REVENUES NEEDED

“We believe there is some risk of further fiscal slippage, given the government’s continued focus on economic growth and the approach of midterm elections in May 2025. The Finance secretary has publicly indicated that no new taxes would be imposed in 2024, and possibly until the end of the Marcos administration in 2028. Nevertheless, we note that overall budget balances have tended to be close to the targets in recent history,” Fitch Ratings said via e-mail.

This highlights the balancing act needed to ensure strong fiscal health, Moody’s Analytics economist Sarah Tan said in an e-mail.

“The government needs funding to provide support for the country to expand, but it also needs to ensure that its debt doesn’t balloon. The million-dollar question is where this source of funding will come from, but the answer is not as straightforward. Ideally, funding should be less reliant on borrowings and more on tax revenue collections. This reinforces a kind of self-sufficiency,” Ms. Tan said.

“However, the current administration appears to be more hesitant towards the creation of new tax revenue streams, which could hinder the country’s fiscal consolidation efforts. But this is understandable as increasing consumption taxes could threaten to stall the country’s growth engine — private consumption.”

Based on the DBCC’s revised medium-term fiscal program, government revenues are expected to grow by 10.3% annually from 2024 to 2028, reaching P6.25 trillion or 16.9% of GDP by the end of the Marcos administration, supported mainly by tax administration reforms.

Meanwhile, government spending is estimated to remain at an average of about 21% of GDP over the medium term, reaching P7.621 trillion by 2028, the DBCC said. The government wants disbursements for infrastructure to reach 5%-6% of GDP to create a multiplier effect on the economy and seeks to invest in programs and projects that promote social and economic transformation.

Revenue collection currently remains “modest” and could be insufficient to fund the government’s spending priorities, which could result in needing to take on more debt to bridge the gap, GlobalSource Partners’ Philippines analyst and former Bangko Sentral ng Pilipinas Deputy Governor Diwa C. Guinigundo said.

There is a “natural limit” to relying on better tax administration to boost revenues, he said. “The Philippine government also needs to strengthen its tax structure by broadening the tax base and making it more progressive.”

“While debt aggregates continue to be manageable, if our revenue effort remains modest and our public expenditure remains substantial, their proportion to GDP and the corresponding debt service burdens could be unsustainable. There ought to be a significant improvement in both higher revenue effort and more modest expenditure programs in the medium term,” Mr. Guinigundo said.

“Our total outstanding debt-to-GDP ratio is a little over 60%, but still manageable. So, we’re okay. But ideally, we should be further reducing this ratio below the internationally accepted threshold,” former Finance Secretary Margarito B. Teves said in a virtual interview.

Mr. Teves noted that the Philippines’ revenue collection is not as efficient as its regional counterparts.

“We also need to figure out whether there are some few tax measures that should be reasonably proposed to Congress for approval.”

Mr. Recto has said they do not plan to introduce new taxes to raise revenues as they want to focus on improving collection efficiency.

The Finance department has only backed the passage of several revenue reforms to boost revenues: the excise tax on pickup trucks and single-use plastics, changes to the mining fiscal regime and the motor vehicle road user charge, and amendments to the Corporate Recovery and Tax Incentives for Enterprises law. These measures remain pending at different levels in Congress. Only the proposed value-added tax on digital service providers has been passed by lawmakers.

STRATEGIC SPENDING

“The sustainability of the debt management trajectory depends on the government’s ability to maintain a balance between borrowing and economic growth,” Asian Development Bank Country Director for the Philippines Pavit Ramachandran said in an e-mail.

The government must continue to implement reforms like optimizing revenue collection through tax reforms and enhancing nontax revenues, which will allow it to invest in key sectors to boost the economy, he said.

“Structural reforms include market liberalization that opens the economy to more foreign investment and trade, and boost growth prospects. The acceleration in public investment, with its high multipliers, continues to lift growth. Strategic investments in infrastructure and key economic sectors can drive economic growth, expanding the revenue base while lowering the debt-to-GDP ratio,” Mr. Ramachandran added.

“Revenue is just one half of the equation. Expenses by the government should also be kept in check. Prudent spending will go a long way in reducing debt,” Moody’s Analytics’ Ms. Tan said. “If we talk about priorities, perhaps in industries that are more exposed to the private sector such as manufacturing or construction, the government should advocate for even more public-private partnerships. This could help reduce the load on public funding. In doing so, more funding can then be allocated to other sectors such as health and education.”

The government must ramp up investments in infrastructure and upskill the labor force to boost economic activity as part of its debt management efforts, GlobalSource Partners’ Mr. Guinigundo added.

“The Philippine government can only be an enabler of business activities. As such, it should concentrate on providing infrastructure, both soft and hard. It should provide quality education at all levels to ensure we have a competitive labor force, a labor force that knows how to leverage technology and digitalization, a labor force that should be the subject of constant reskilling and upskilling,” he said. “On hard infrastructure, it should concentrate on establishing both physical and communication connectivity. The Philippines is an archipelagic country and therefore transportation infrastructure is most critical.”

“If we are able to boost business activities in a big way, then we can also nurture exports and win big in foreign exchange earnings. That should help us service foreign debts,” Mr. Guinigundo said. — Beatriz Marie D. Cruz

{kind=link}